Banking has had to chart a challenging course over the past few years, during which institutions faced increased oversight, digital innovation, and new competitors, and all at a time when interest rates were at historic lows. The past few months have also brought their share of upsets, including liquidity woes and some bank failures. But, broadly speaking, a favorable wind seems to have returned to the industry’s sails. The past 18 months have been the best period for global banking overall since at least 2007, as rising interest rates have boosted profits in a more benign credit environment.

About the authorsThis report is a collaborative effort by Debopriyo Bhattacharyya, Miklós Dietz, Alexander Edlich, Reinhard Höll, Asheet Mehta, Brian Weintraub, and Eckart Windhagen, representing views from McKinsey’s Global Banking Practice.

Below the surface, too, much has changed: balance sheet and transactions have increasingly moved out of traditional banks to nontraditional institutions and to parts of the market that are capital-light and often differently regulated—for example, to digital payments specialists and private markets, including alternative asset management firms. While the growth of assets under management outside of banks’ balance sheets is not new, our analysis suggests that the traditional core of the banking sector—the balance sheet—now finds itself at a tipping point. Given the size of this movement, we have broadened the scope of this year’s Global Banking Annual Review to define banks as including all financial institutions except insurance companies.

In this year’s review, we focus on this “Great Banking Transition,” analyzing causes and effects and considering whether the improved performance in 2022–23 and the recent rise in interest rates in many economies could change its dynamics. To conclude, we suggest five priorities for financial institutions as they look to reinvent and future-proof themselves. The five are: exploiting leading technologies (including AI), flexing and potentially even unbundling the balance sheet, scaling or exiting transaction business, leveling up distribution, and adapting to the evolving risk landscape.

All financial institutions will need to examine each of their businesses to assess where their competitive advantages lie across and within the three core banking activities of balance sheet, transactions, and distribution. And they will need to do so in a world in which technology and AI will play a more prominent role, and against the backdrop of a shifting macroeconomic environment and heightened geopolitical risks.

White labyrinth balls skillfully navigate a vibrant yellow maze, serving as a visual metaphor for the journey of success, progress, and motivation, complete with its highs and lows.

The recent upturn arises from the sharp increase in interest rates in many advanced economies, including a 500-basis-point rise in the United States. The higher interest rates enabled a long-awaited improvement in net interest margins, which boosted the sector’s profits by about $280 billion in 2022 and lifted return on equity (ROE) to 12 percent in 2022 and an expected 13 percent in 2023, compared with an average of just 9 percent since 2010 (Exhibit 1).

Over the past year, the banking sector has continued its journey of continuous cost improvement: the cost-income ratio dropped by seven percentage points from 59 percent in 2012 to about 52 percent in 2022 (partially driven by margin changes), and the trend is also visible in the cost-per-asset ratio (which declined from 1.6 to 1.5).

The ROE growth was accompanied by volatility over the past 18 months. This contributed to the collapse or rescue of high-profile banks in the United States and the government-brokered takeover of one of Switzerland’s oldest and biggest banks. Star performers of past years, including fintechs and cryptocurrency players, have struggled against this backdrop.

Performance varied widely within categories. While some financial institutions across markets have generated a premium ROE, strong growth in earnings, and above-average price-to-earnings and price-to-book multiples, others have lagged (Exhibit 2). While more than 40 percent of payments providers have an ROE above 14 percent, almost 35 percent have an ROE below 8 percent. Among wealth and asset managers, who typically have margins of about 30 percent, more than one-third have an ROE above 14 percent, while more than 40 percent have an ROE below 8 percent. Bank performance varies significantly, too. These variations indicate the extent to which operational excellence and decisions relating to cost, efficiency, customer retention, and other issues affecting performance are more important than ever for banking. Strongest performers tend to use the balance sheet effectively, are customer centric, and often lead on technology usage.

Between 2017 and 2022, payment providers, capital market infrastructure providers, and asset managers, as well as investment banks and brokers-dealers increased their price to earnings, whereas other financial institutions including GSIB (global systematically important banks), universal banks, and nonbank lenders saw a decline in their price to earnings.

Payment providers, investment banks and broker dealers also increased their earnings per share more than the other types of institutions. Consequently, these two types of institutions come out best in terms of value creation and total return to shareholders among financial institutions during this five-year period.

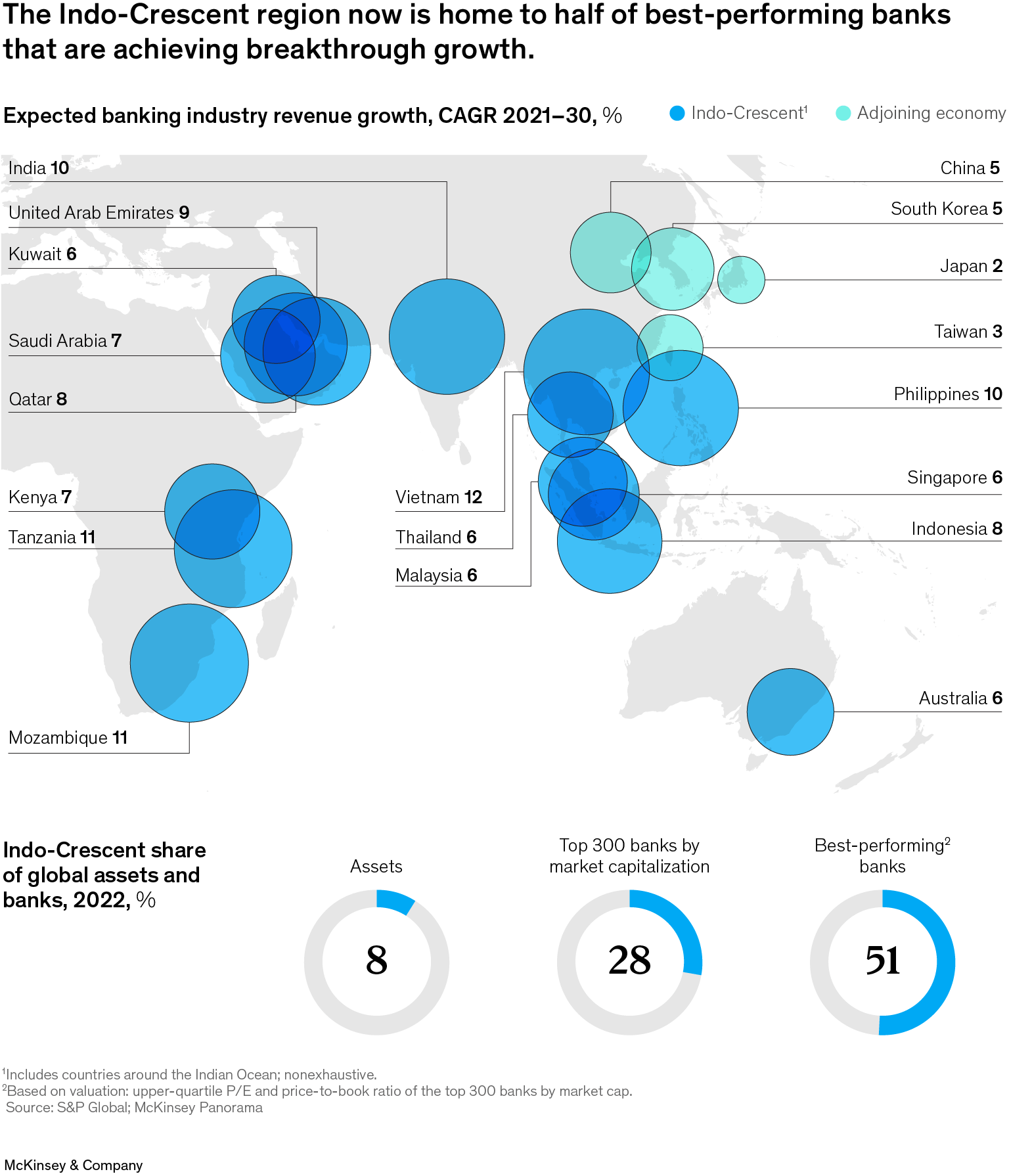

The geographic divergence we have noted in previous years also continues to widen. Banks grouped along the crescent formed by the Indian Ocean, stretching from Singapore to India, Dubai, and parts of eastern Africa, are home to half of the best-performing banks in the world (Exhibit 3). In other geographies, many banks buoyed by recent performance are able to invest again. But in Europe and the United States, as well as in China and Russia, banks overall have struggled to generate their cost of capital.

half of best-performing banks that are achieving breakthrough growth." />

half of best-performing banks that are achieving breakthrough growth." />

One aspect of banking hasn’t changed, however: the price-to-book ratio, which was at 0.9 in 2022. This measure has remained flat since the 2008 financial crisis and stands at a historic gap to the rest of the economy—a reflection that capital markets expect the duration-weighted return on equity to remain below the cost of equity. While the price-to-book ratio reflects some of the long-term systematic challenges the sector is facing, it also suggests the possible upside: every 0.1-times improvement in the price-to-book ratio would cause the sector’s value added to increase by more than $1 trillion.

Looking to the future, the outlook for financial institutions is likely to be especially shaped by four global trends. First, the macroeconomic environment has shifted substantially, with higher interest rates and inflation figures in many parts of the world, as well as a possible deceleration of Chinese economic growth. An unusually broad range of outcomes is suddenly possible, suggesting we may be on the cusp of a new macroeconomic era. Second, technological progress continues to accelerate, and customers are increasingly comfortable with and demanding about technology-driven experiences. In particular, the emergence of generative AI could be a game changer, lifting productivity by 3 to 5 percent and enabling a reduction in operating expenditures of between $200 billion and $300 billion, according to our estimates. Third, governments are broadening and deepening regulatory scrutiny of nontraditional financial institutions and intermediaries as the macroeconomic system comes under stress and new technologies, players, and risks emerge. For example, recently published proposals for a final Basel III “endgame” would result in higher capital requirements for large and medium-size banks, with differences across banks. And fourth, systemic risk is shifting in nature as rising geopolitical tensions increase volatility and spur restrictions on trade and investment in the real economy.

A mesmerizing display of multi-colored cubic shapes with interconnected curved concave elements, forming an intricate path where numerous labyrinth balls skillfully maneuver, embodying the concept of a transformative journey.

In this context, the future dynamics of the Great Transition are critical for the banking sector overall. Evidence of the transition’s profound effect on the sector to date abounds. For example, between 2015 and 2022, more than 70 percent of the net increase of financial funds ended up off banking balance sheets, held by insurance and pension funds, sovereign wealth funds and public pension funds, private capital, and other alternative investments, as well as retail and institutional investors (Exhibit 4).

The shift off the balance sheet is a global phenomenon (Exhibit 5). In the United States, 75 percent of the net increase in financial funds ended up off banking balance sheets, while the figure in Europe is about 55 percent.